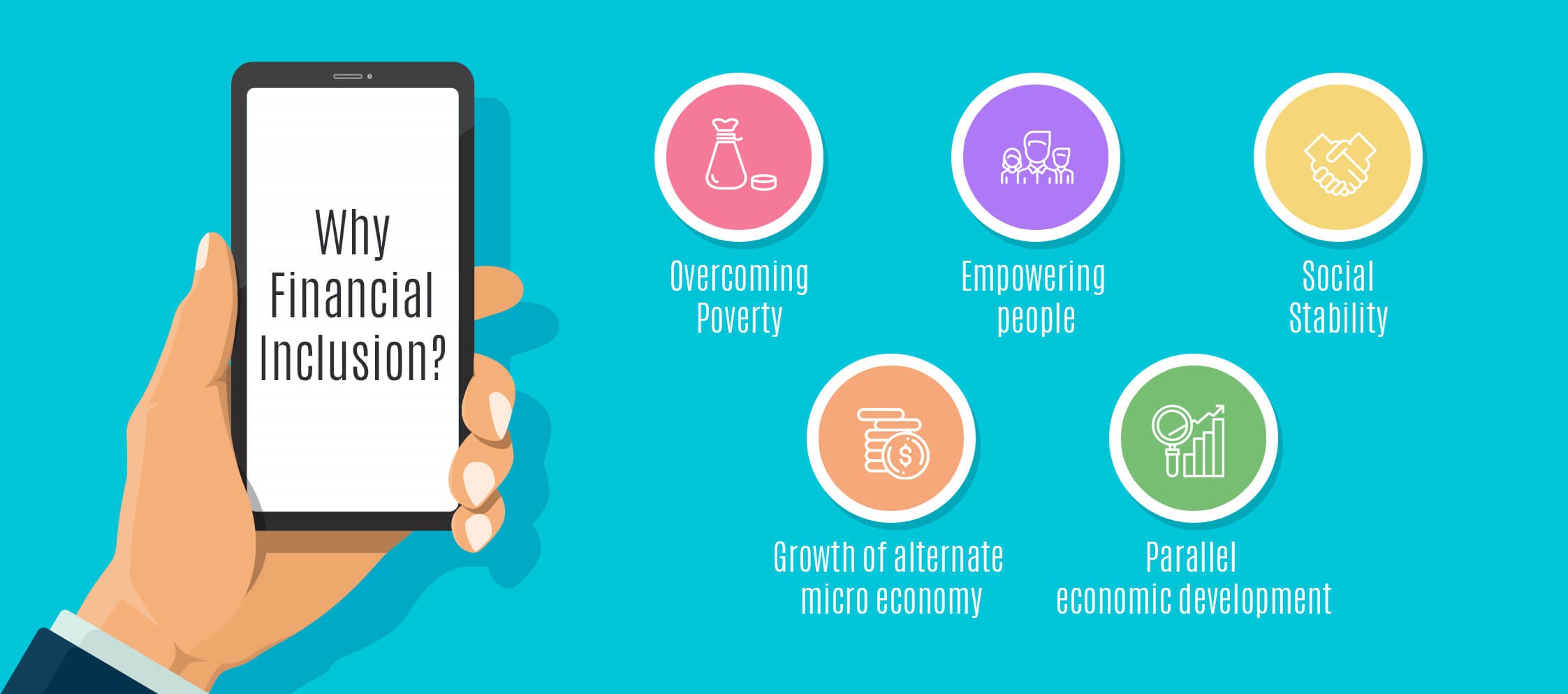

Economic inclusion, or having access to formal financial services like bank accounts, credit, and loans, is one of the most effective ways to end poverty cycles. Unfortunately, as many as 1.7 billion individuals worldwide still need bank accounts or access to financial services. Those already economically vulnerable will find it more challenging to improve their circumstances because of this condition. Fortunately, AI and blockchain are only two examples of cutting-edge technology bringing novel approaches to expanding people’s access to formal money.

Technology can foster inclusiveness by enabling new ways of working, such as through digital labour platforms, and removing barriers to employment, such as long commutes. Furthermore, beyond the workplace, technology may promote educational achievements at all levels and enable more efficient retraining, thereby expediting the adoption of innovations to increase productivity and expand enterprises. All of this can contribute to the global labour force being more fully used, reducing the gender wage gap, and bringing about a more thriving and sustainable economy for all of us.

Technology’s Role in Progressing the Economy

Business Globalization:

Because of the advancements in business technology, it expanded its operations internationally. Today, trade between countries is a breeze. Thanks to technological advances, internet commerce has flourished, injecting fresh energy into corporate globalization. In addition, the widespread adoption of information technology has dramatically facilitated economic globalization by lowering production network costs and increasing accessibility.

Increased Productivity:

The economy has grown and increased its output thanks to technological advancements. This result is a result of the efficient use of labour and technology in the manufacturing sector of the global economy.

Future Opportunities for Technology

- Artificial intelligence will generate enormous value

According to a Mckinsey report, artificial intelligence (AI) can add up to $1 trillion to the global banking industry yearly. Leaders in the banking industry are transforming their operations through the organic application of AI throughout the whole lifecycle of their digital operations.

The financial industry realizes algorithms are only as good as the data inserted in them. As a result, the focus is shifting to establishing a competitive advantage from previously underutilized consumer behaviour data obtained through traditional operations.

This will unleash the previously untapped potential of ecosystem-based financing, in which banks, insurers, and other financial services organizations collaborate with non-financial players providing client experiences in areas beyond their conventional remit.

2. Blockchain will upend traditional financial conventions.

A new digital form of a country’s fiat currency issued directly by the country’s monetary authority or central bank is expected to have one of the most major disruptive effects in the next 3-5 years. This is a digital currency issued by a central bank (CBDC).

A CBDC, supported by blockchain technology, can transform the financial system, paving the path for greater financial inclusion and improving the lives of billions of people worldwide by offering access to low and affordable financial services. A well-designed CBDC, owing to its architecture, can support offline payments, protected transfers, automation throughout the programmability layer, and cash-like features.

Combined, these characteristics will promote the user’s financial inclusion by providing a digital alternative to physical cash, improving access to their money even in remote places, and providing coherent options for currently unbanked people.

3. Cloud computing will unleash participants in the financial services industry.

Cloud computing frees financial institutions from non-core activities while providing flexible storage and computing services at a reduced cost. Simultaneously, the cloud is giving rise to new formats, such as open banking and banking-as-a-service, which are upending the age-old relationship between customers and financial service providers.

Financial institutions, such as banks, will continue to rely on the cloud as they recognize the opportunity to adopt cloud-based micro-service architecture in the following years, where application programming interfaces (APIs) allow machine-to-machine transmission and allow services to scale individually without extending the overall offering’s coding base.

4. The Internet of Things will usher in a new era of financial trust.

In banking, IoT-based inventory and property finance improve risk administration by verifying that accounting records match real-world transactions, allowing for the latest trust structure.

IoT is shaking up conventional trade financial affairs in shipping and planning, allowing banks to build contemporary products based on commodities movement trackings, like on-demand liquidity and other innovations delivered via smart agreements.

Another method that IoT is bringing financial institutions closer to their clients is by fixing financial services, such as digital payments, inside wearables. Meanwhile, insurers leverage IoT to assess risk better, improve consumer engagement, and streamline the claims process.

5. Open source, SaaS, and serverless will lower entry barriers.

For technology players and traditional financial institutions developing the latest fintech organizations, open-source software, serverless architecture, and software-as-a-service (SaaS) have become necessities.

SaaS allows businesses to use the software as needed without owning it. In contrast, serverless architecture removes the need for companies to run their servers, freeing up time and resources for customers and operations. The serverless design also saves money because charges are tied to executed software code rather than being generated continuously, independent of business requirements. It also promotes flexible scaling, which reduces idling and loss while increasing development efficiency.

6. No-code and low-code will radically alter application development.

No-code development platforms (NCDPs) and their close cousin’s low-code platforms enable non-programmers to create applications using graphical user interfaces rather than traditional computer programming.

Enterprises commonly use NCDPs to accelerate building cloud-based apps while maintaining business strategy alignment. For example, compliance can be improved by automating audit trails and document generation on no-code or low-code systems. This is highly beneficial for financial institutions and fintech start-ups that need to adapt swiftly to market movements.

Conclusion

As populations age and growth slows, there are unrealized economic potentials that could make a significant impact. Innovation is a crucial strategy to spur growth and contribute to Economic Inclusion’s goal of bringing in previously excluded groups from the labour market. Although advancement is gradual and inconsistent across nations, politicians and businesses may be eager to embrace inclusion as a desirable and necessary approach as they recognize that the steady drop in the working-age population in most industrialized countries is a headwind to growth. We anticipate that Technological innovation will play a pivotal role in driving this change.