Small and medium-scale enterprises are intensely involved with the economy of the nation. Some of the time, they also play a pivotal role in pushing up the economic growth of a country. But in most cases, SMEs face many financial obstacles, such as arranging capital to start or running the business smoothly. We can all agree that financial flow is always necessary for running or growing a business. To supplement their economic scarcity, SMEs typically apply for loans, but they are met with heartbreaking denials.

In some cases, SMEs are responsible for denials of loans; lack of performance, previous business dealings, and eagerness to repay the loan all play a significant part. Because any company, bank, or personal creditor will not provide money without any background check. So first, try to be in the investors’ good books.

Discuss such issues and some easy remedies to overcome the hard times.

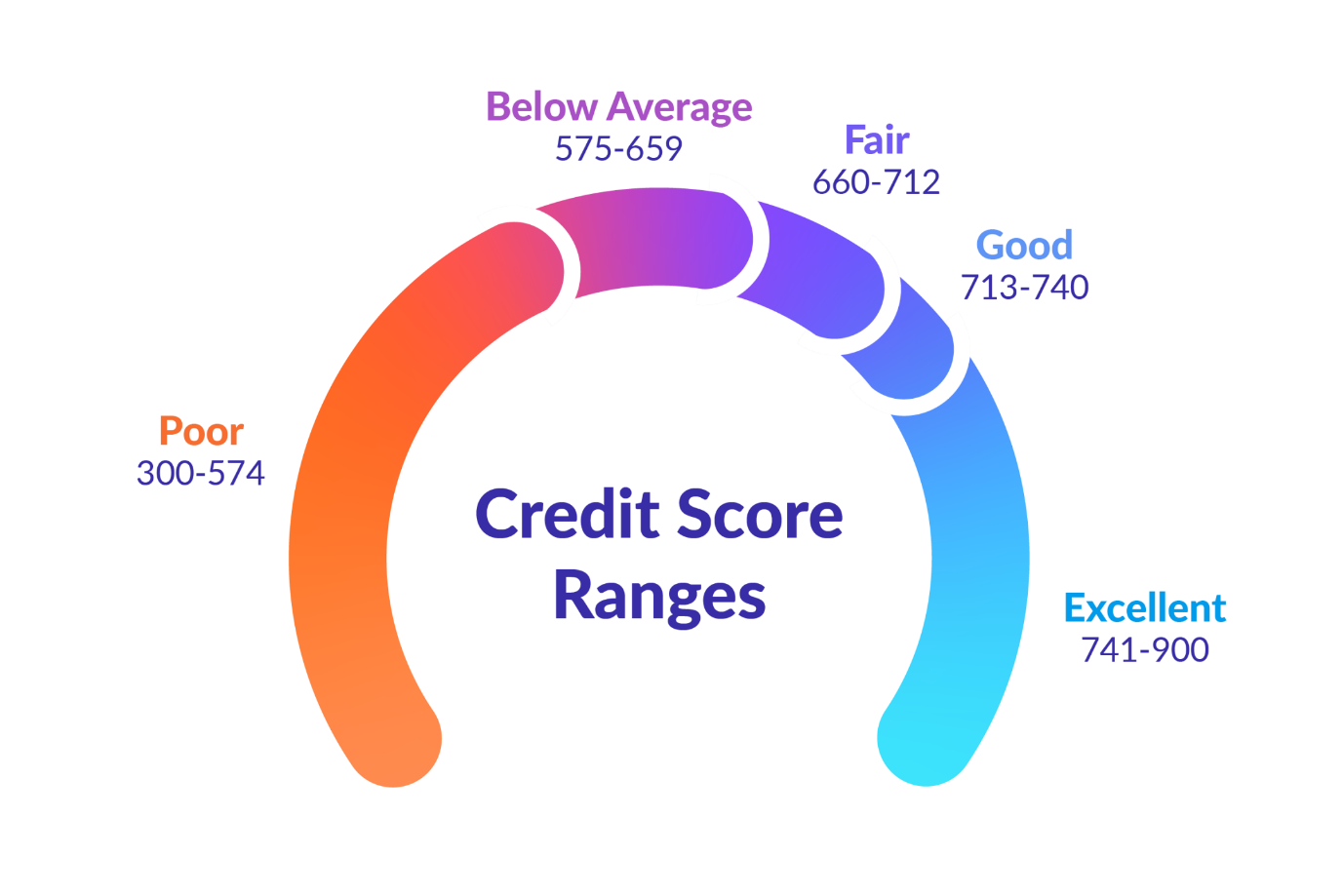

- Credit score

SMEs have to be well researched in credit score and credit history. In a nutshell, this is the magical password to obtaining credit; the credit score is data that can be used to assess a person’s or business’s creditworthiness. Without a good credit score, getting loans would not be easy, so before applying for a loan, SMEs must sort out all previous monetary dealings and court judgments, if there are any. The abundance of loans on the market may hurt loan availability because it will affect one’s credit score. Low credit scores are the most common reason for the denial of loans. A low credit score indicates that it would be troublesome for the creditors to repay the loan amount. So creditors will not be ready to grant the loan out of uncertainty.

- History of business dealings

Banks and other financial companies that provide loans to SMEs collect data from the market and the history of previous monetary dealings before granting credit because it is risky for the creditors. However, it is their business to make loans at a high-interest rate. They must be sure first about the eligibility of the SMEs to repay. Credit and debit are the most critical factors in granting a loan. SMEs also have minimal mortgage options due to the limited resources of their small-scale industries.

Always try to maintain a good term with the investors and repay the debt on time. Keeping an organized official record of your business transactions; without one, it would be difficult to get credit.

- Necessary cash flow in business

Small and medium-sized businesses may struggle to produce documents demonstrating good cash flow to run the business or well-established business growth. This low cash flow is a wrong signal for small-scale entrepreneurs trying to get loans. Maintaining a good cash flow is always tricky, even if they are profitable. They must retain cash liquidity with suppliers and workers before they are paid for the product or service. Workers and suppliers are the pillars of business. If the investors get unsatisfied credentials, they will turn down the loan.

In the world of business, everybody works for a profit. Investors invest their hard-earned money to get a profit, and SMEs channelize the invested amount for their production and business growth. Improper business maintenance and the inefficient governing body of SMEs might be the reasons for turning down the application for the loan. As a result, entrepreneurs must demonstrate their sincerity and ability to advance the business through proper management. It is a critical factor for new and small-scale industries.

- Investor constraints; high-risk factor

In recent times, the industry has witnessed some bankruptcy. Small and medium-sized businesses are always a risk for investors. They hesitate to invest in SMEs or startups because it’s like gambling; there is uncertainty about getting back the investments.

Any bankruptcy-like situation on the credit profile is a dangerous signal. The application for a loan might be rejected. But do not be hopeless; it doesn’t mean SMEs will not get a loan in the future borrowing. Sometimes, SMEs also get credit from another risk-taking lender. If one can show positivity and productivity, one may get a loan, though there are a lot of difficulties. Try to remove the bankruptcy tag from the business profile by achieving some positive goals. Try to obtain a secured credit card, or enlist yourself as a member of a credit union. Arrange a co-signer to re-claim the credit and put the business on the desired track.

- Inappropriate Loan Application

Lastly, an inappropriate loan application or preliminary official paperwork might be a reason for rejecting the loan application. Most loans providing financial institutes are not eager to give loans to SMEs. So, they can quickly leave the plea if they discover flaws in their documentation review. An incomplete application in every aspect will be denied; this may exhibit the inefficiency of paperwork or conceal information. Both create a negative attitude towards the investors.

Try to provide all the necessary documentation along with the loan application, such as bank statements, legal documents, tax returns, and financial statements. If the investors want to know about the future business plan, provide them with the plan in a more easy-to-understand and organized way. One will be in a higher position than others if they can convince the investors through clarity of information and proper planning. One has to be cautious about filling out the application.

Some important notes for the betterment of SMEs

- Always try to pay the monthly bills or any other periodical transaction on time. Timely payments of the debts or bills ensure the borrower’s capability and potential trustworthiness. No one keeps faith in the defaulters. Timely payment will represent punctuality and save the late fee as well.

- It will be helpful in the future if the entrepreneur maintains lower credit utilization limits. It would be a good sign to get a loan from the lenders. Frequent borrowers may not get loans quickly because some investors think it might be a habit of lending.

- Do not apply multiple times for a loan in a short period. This may represent stubbornness or stress. Numerous credit inquiries on the business account within a short period can hurt the business profile.

- Try to avail government-aided schemes; one can get a loan at a low-interest rate.

If one gets multiple loan rejections, it might be stressful. But always believe in the personal potential and keep our heads; be a phoenix, start fresh. Try to assemble the lessons from the previous mistake.