After strategy, value creation is said to be the most abused and loosely used phrase in management jargon! And yet its importance can’t be underestimated as value creation has, and will remain the ultimate goal for any business. Let’s understand why. If we take the example of startups, the Toast of India Inc – 100 plus unicorns had a total valuation of $349.67 Bn in October 2023. Out of these, some like Byjus, Ola, and Swiggy saw a markdown of 49% in their valuations. Byju’s valuation of $22 bn has now dropped to a mere $1bn!

Entrepreneurship is often seen as more about valuation and not value creation. Profit maximization – the primary purpose of any business – without creating value is devoid of purpose. Value creation based on futuristic growth strategy is not only the springboard but also the foundation of a successful enterprise.

How do we define value creation in tangible terms?

An abstract concept like value creation can be best explained by taking inspiration from Jim Collin’s bestseller Good to Great – it is an organisation’s journey and transition from good to great; It is what distinguishes some enterprises that leap from those that don’t and why the mighty fall.

To go deeper, value creation can be described as a set of behaviours, norms, and processes a company adopts to achieve superior results, build lasting competitive advantage and create new successful revenue streams to build scale and profitability.

Fundamentally Value creation goes beyond obvious balance sheet metrics like revenue and profitability to, among others – embracing change for growth, an ability to foster a culture of consistent high performance, innovation, and continuous improvement in efficiencies, building a strong brand reputation and strategic partnerships, employee satisfaction and retention, compliances with corporate gov norms and adapting to evolving customer needs in a VUCA world

MSME 2.0: The Numbers tell a story

In the post-COVID world, there is a buzz about MSME 2.0, and no doubt, the sector has shown encouraging signs of revving up. The MSME sector is called the backbone of the economy but numbers tell a different story. While post-pandemic the sector is showing signs of energy, the fact is that the gap between expectations from this sector vs its current challenges is humongous.

Although the MSME sector accounts for 30% of the GDP and 40% of the exports, fragmentation, lack of formalisation/lack of scale have been the bane of this sector. Out of the 63 million enterprises, more than 90% are micro-enterprises with less than 5 cr turnover, several small enterprises are around 6-7% (with 50 cr + turnover) and medium enterprises (with 250 cr + turnover) would be not more than 2-3%.

Unless we can get more SMEs to scale up and transition from micro to small and medium, our goal of becoming a $ 5 trillion economy by 2026 will only be deferred.

India’s goal of becoming a $ 5 trillion economy is unlikely to happen without a vibrant MSME sector. That’s where MSME 2.0 becomes an imperative. Unless enterprises develop the skills and the capability to scale and expand exponentially, the MSME 2.0 story may never take off. And Value creation becomes the only route to achieve this

Where are the bottlenecks?

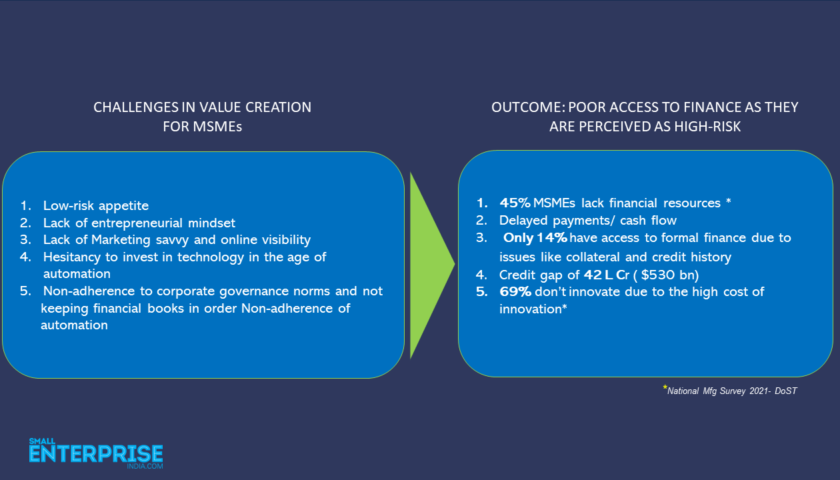

While access to finance, the lifeblood of any business, is the biggest challenge for the sector it is at best symptomatic of the larger macro challenges which need to be addressed for MSME 2.0 to take off.

But in the Industry 4.0 scenario and the digital age, the challenges for SMEs are many – from shifting expectations of the Millennial and Gen Z customers, adapting to an era of digital disruption and green transition to managing a hybrid workforce and enabling them with new skill sets are only some of the challenges that organisations face. This is why Value Creation becomes non-negotiable in an SME’s growth journey.

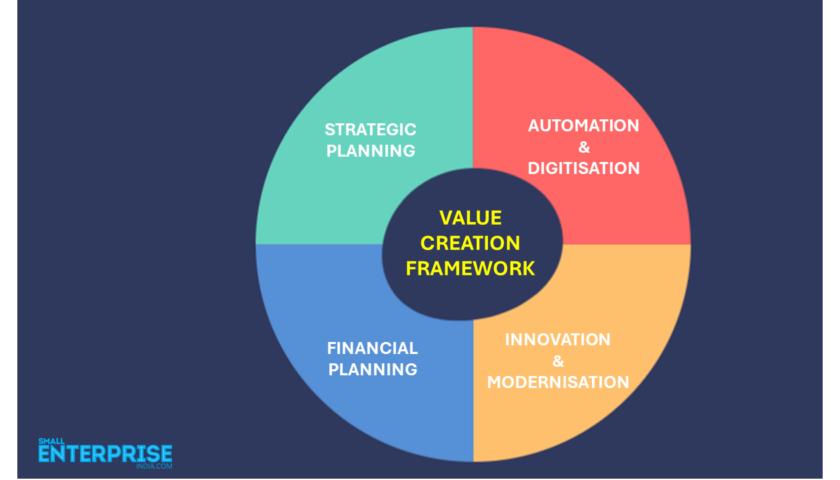

The Value Creation Template for MSME: How to create value and build scale?

If Finance, as the lifeblood of any business, is the biggest hurdle for micro and small enterprises, then Financial Planning is undoubtedly one of the key pillars of value creation.

In the disruptive digital era, the whys, hows, and whats of any business are not unidimensional and are far more complex and constantly evolving. Therefore, value creation needs to be seen from multiple prisms. The Value Creation template therefore for MSME operates on four key components which need to work synergistically.

1. Go Digital for Data-driven decision-making

Automation by embracing digital tech across functions is at the heart of the Value Creation Strategy. Helps in the simplification of processes, eliminates manual work improves margins and performance, and reduces risk.

Automate/ Digitise operationsfor seamless data migration across platforms and functions with cloud-based technology to integrate Financial and Customer Information into one system and align all functions (ERP integration – Invoicing, Accounting, Purchase, Production, Inventory, CRM (Marketing Sales), and Payroll.

Customer Centric Approach – Streamline customer relationships with CRM tools

Be visible online and build your public profile2. Financial Management for risk /cost optimisation & resource planning

Finance once a Cost Centre, now has a critical role in Performance Management by developing KPIs that align with Objectives and help track progress, management reporting, Planning and forecasting, and cashflow/revenue projections.

Leveraging Digital lending/ Fintech solutions like Supply Chain/ invoice financing, reverse factoring, cashflow-based credit, collateral-free loans for cashflow, and working capital management.

Moving from asset-based or balance sheet-based lending to cashflow-based digital lending for small ticket loans to manage WC and invest in growth.

Vendor financing and exploring access to private capital from VCs/Equity funding.

Improving Corporate Governance Reporting and Compliance.

3. Innovation and Modernisation

In a globalised and disruptive world – Innovation (be it in terms of ideas, new markets, customer segments, competitive advantage, product offerings, processes, new age technology) and modernization (of manufacturing equipment and processes, technology transfer, adoption of global best practices and ESG norms as part of the corporate strategy) has to be an integral part of the value creation strategy.

4. Strategic Thinking and Planning

Getting the basics right –

Having the right answers to the whos, whats, and hows of your business which are constantly evolving in a disruptive age

Your vision for the business how are you going to get there and what does it cost? Where do you see your business in the next 5 years?

Knowing your markets, the nature of disruption, and how it is impacting your business, your competition, and customer trends and expectations.

Opportunity Assessment – where is growth going to come from? Existing or new businesses?

Summing Up: The Big Picture and Value Creation Opportunity for MSME

To sum up, while MSMEs contribute around 30% to the GDP, the sector would need to grow exponentially to be able to drive the economy to touch the $ 5 trillion mark. It is in this context that one needs to closely scan the opportunity landscape to see which are the low-hanging fruits that can be leveraged to ensure its value creation efforts deliver positive and tangible outcomes. For an enterprise, as it gets focused on the nuts and bolts of the value creation strategy and its execution and operations, it is important to not lose sight of the Big Picture and see the Opportunity landscape.

1. Fintech Revolution – led by digitisation of the financial ecosystem is driving massive transformation in we do business and in lowering the cost of credit and enabling ease of access to low-cost, hassle-free finance for MSMEs.

- India is setting the template for the rest of the world with its innovative models in fintech and financial services. Our fast-growing digital population, world-class digital public infrastructure (DPI), Govt’s mandate on e-invoicing, and proactive regulators ( RBI/SEBI/Ministry) are key tailwinds driving fintech growth, which will expand into a $400 billion opportunity by 2030 as per a Mckinsey study.

- Supply Chain/Vendor Financing( reverse factoring) where MSME suppliers can receive payment against invoices from corporates/lenders.

- Cash flow or Invoice financing based on past and projected cashflow which is collateral-free and avoids risk assessment (FINNOVATE: FinTech for SMEs – 22 February’24, Bangalore – REGISTER NOW)

2. Best time to go Global

In an era of borderless commerce, Global expansion is a huge opportunity for MSME in today’s interconnected world. Going global for MSMEs gives an opportunity to access a larger customer base and new technologies. The New FTB ( Foreign Trade Policy ) targets $2 trillion in total exports by 2030 to achieve its larger goal of $ 5 trillion for the economy and aims to empower MSMEs by providing them with a level playing field to compete with larger players in the global market – with incentives and support to enhance their exports by way of reduction of compliance costs for exporters and simplification of the export procedures and inclusion of ECGC Limited scheme for small exporters to reduce costs and access export credit insurance.

For MSMEs who are already contributing 40% to India’s exports, this is a humongous value-creation opportunity to establish scale and get cross-border growth.

Another game changer for MSMEs in the new FTO is the focus on promoting Cross Border Trade through e-commerce exports by providing MSMEs with access to international e-commerce platforms.

3. E-Commerce: The Catalyst for MSME growth in cross-border trade

The consumer internet economy or E-Commerce market is expected to touch $ 1 trillion by 2030 according to a Google, Bain, and Temasek report. With 700 million internet users transacting more via real-time digital payments and spending more time on online video streaming services and social media than global averages, the internet economy is set to expand beyond its current base. Although this will be led by the B2C segment, the B2B segment is expected to touch $ 60 billion by 2025 (Statista) driven by cross-border trade.

Several AI-backed platforms today enable SMEs to gain cross-border presence and visibility with ease of doing business internationally by streamlining shipping operations, providing logistical (order fulfillment services) and supply chain solutions for order fulfillment at a lower cost thereby offering a seamless digital experience – as customer journey in E-Commerce doesn’t stop at purchase confirmation

Adopting a digital and automated supply chain ecosystem is the best way to gain a competitive advantage in the B2B industry to provide customers with efficient transparent order management, make data-driven decisions with the facility of real-time changes, delivery process automation, tracking and tracing orders and help measure SLA compliance.

4. Leverage Govt Incentives and Programs to maximise gains

- MSMEs, grappling with day-to-day operations and nuts and bolt issues, need to take advantage of the supportive and proactive role played by the Govt in trying to build an enabling ecosystem for MSME through various Flagship schemes like Atmanirbhar Bharat, PLI scheme, etc – the lack of awareness of which may prevent them from benefits it can derive.

- Mandate on compulsory e-invoicing has been a big enabler in the digitisation of supply chain financing and the fintech revolution.

- ONDC – Open Network For Digital Commerce (ONDC) – a mega initiative that will democratise digital commerce the way UPI revolutionalised digital payments and provide a level playing field to E-Commerce platforms and facilitate seamless integration and movement across platforms.

· OCEN – Open Credit Enabled Network works in tandem with AA (Account Aggregators) and provides digitised credit infrastructure and enables cashflow-based lending without collaterals and helps fintech players to build cashflow based lending products and enable underwriting of credit by Banks and NBFCs. It also furthers partnerships between digital platforms and lenders or LSPs (lending service providers) thus reducing the high cost of borrowing and lowering the turnaround time for loan disbursement.

- Udyam Portal a single window for free paperless registration of MSMEs which is integrated with GST and IT for ease of doing business and gives eligibility to avail schemes and subsidies as well collateral-free low-interest loans etc.

This brings the informal sector under the formal ambit for availing benefits under Priority Sector lending (PSL).

- RAMP (Raising and Accelerating MSME performance) is a World Bank-assisted scheme to incubate, innovate, and support new businesses.

- TReDs -Trade Receivables Discounting system is an electronic platform under RBI for discounting/financing trade receivables through multiple financiers. TReDs have resulted in a lower cost of financing as they rely on the Buyer’s credit, and facilitate better working capital management as companies can avail finance against invoices within 24 hours.

5. Go Public to raise funds for investing in long-term growth

Strong participation from family firms and HNIs has led to a boom in MSMEs exploring the IPO market for raising funds with 139 MSMEs raising 3500 cr.

In conclusion

We need to see more MSMEs transforming into unicorns, but valuations alone are not enough; they must ‘add value’ too to become a potent growth engine of the economy!

MSMEs, by embarking on a value-creation initiative can truly help the Indian economy to become self-reliant. They hold the potential to transform the economy, foster job creation, and promote equitable economic growth with the support of the Govt in creating an enabling ecosystem and infrastructure

Globally while MSMEs account for 90% of businesses and 50% of GDP, in India they account for less than 30% of the GDP. That’s the gap that value creation initiatives can fill. We need more enterprises to migrate from micro to small, from small to medium, and from medium to big. As this transition happens, a plethora of opportunities will open up and they will be able to attract larger investments, adopt cutting-edge technology, and participate in global supply chains – thereby contributing to domestic manufacturing. India’s hopes of reaping the benefits of a China plus One Strategy depends to a large extent on how quickly the MSME sector becomes one of the growth engines of the economy.

Author: Jyoti Shiralee is the Founder and Director of Chrysalis Consulting, a Mumbai-based growth advisory that works with the MSME sector. She can be reached at jyoti@chrysalisconsulting.co.in